Delap Wealth Advisory’s evidence-based investing portfolios are strategically invested with a focus on long-term performance objectives. Portfolio allocations and investments are not adjusted in response to market news or economic events; however, we evaluate and report on market and economic conditions to provide our investors with perspective and put portfolio performance in proper context.

Global stock markets continued to rebound during the third quarter of 2020 and are still working to recover losses from the first quarter in most areas of foreign and domestic markets. This positive performance follows continued global efforts to reopen economies under social distancing guidelines during the quarter. While we cannot say with certainty what caused markets to move, the Fed’s new inflation-targeting policy, relative outperformance among equities in the technology sector, and the nearing of the U.S. presidential election all contributed to market growth and volatility.

For the quarter, U.S. stocks (as measured by the S&P 500 Index) gained 8.9%, and non-U.S. developed market stocks (as measured by the MSCI World Ex U.S.) gained 4.9%. Emerging market stocks (as measured by the MSCI Emerging Markets Index) gained 9.6%.

The U.S. Dollar Index, a measure of the value of the United States dollar relative to a basket of foreign currencies, decreased in the third quarter — the U.S. dollar decreased by 3.6% compared to foreign currencies. Over the past 12 months, the U.S. dollar depreciated by 5.5%. The decrease in the dollar is a tailwind to non-U.S. investments held by U.S. investors in the third quarter.

U.S. interest rates remained unchanged during the quarter as the Federal Reserve continues to maintain a target range of 0.0% to 0.25% for the Fed Funds rate. Since changes in interest rates and bond prices are inversely related, continued low interest rates helped increase the quarterly return for many bond asset classes.

U.S. Economic Review

The U.S. economy continued to contract as the year progressed. The final reading for second quarter 2020 GDP showed an annualized decline in economic growth of 31.4%, which is the largest percentage decline on record. The unemployment rate finished the quarter at 7.9%, which shows improvement from the previous quarter’s 11.1%. Domestic inflation remains low as the Fed’s preferred gauge of overall inflation, the core Personal Consumption Expenditures (PCE) index, stayed below the Fed’s target of 2.0% with a reading of 1.6% in August 2020.

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, U.S. Department of the Treasury, Morningstar Direct October 2020.

Financial Markets Review

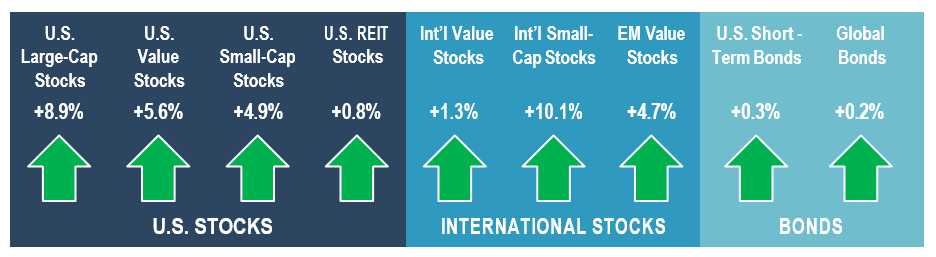

Both domestic and international stocks across all size and style categories, as well as U.S. real estate investment trust (REIT) securities, had positive performance during the quarter. International stock returns were also impacted by the weakening U.S. dollar. During the quarter, international small-cap stocks were the best performing and U.S. REIT securities were the worst performing. U.S. and global bonds continued performance from the previous quarter by posting positive results.

Source: Morningstar Direct October 2020. Market segment (Index representation) as follows: U.S. Large-Cap Stocks (S&P 500 Index), U.S. Value Stocks (Russell 1000 Value Index), U.S. Small-Cap Stocks (Russell 2000 Index), U.S. REIT Stocks (Dow Jones U.S. Select REIT Index), International Value Stocks (MSCI World Ex USA Value Index (net div.)), International Small-Cap Stocks (MSCI World Ex USA Small Index (net div.)), Emerging Markets Value Stocks (MSCI Emerging Markets Value Index (net div)), U.S. Short-Term Bonds (ICE BofA 1-3Y US Corp&Govt TR), Global Bonds (FTSE WGBI 1-5 Yr Hdg USD).

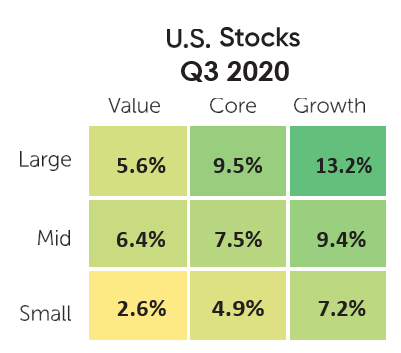

In the U.S., large-cap stocks outperformed small-cap stocks in all style categories. Value stocks underperformed growth stocks in all style categories. Among the nine style boxes, large- cap growth stocks performed the best and small- cap value stocks experienced the least growth during the quarter.

Source: Morningstar Direct October 2020. U.S. markets represented by respective Russell indexes for each category (Large: Russell 1000, Value, and Growth, Mid: Russell Mid Cap, Value, and Growth, Small: Russell 2000, Value, and Growth).

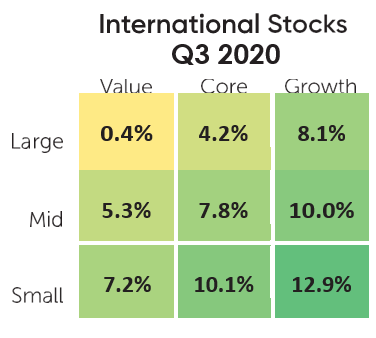

In developed international markets, all nine style boxes were positive for the quarter. International small growth stocks were the highest performer. In contrast to the U.S., international small-cap stocks outperformed large-cap stocks across all styles.

Source: Morningstar Direct October 2020. International markets represented by respective MSCI World EX USA index series (Large: MSCI World EX USA Large, Value and Growth, Mid: MSCI World Ex USA Mid, Value, and Growth, Small: MSCI World Ex USA Small, Value, and Growth).

A diversified index mix of 65% stocks and 35% bonds would have gained 3.5% during the third quarter.

65/35 Index Mix: 0.5% Cash (ICE BofA 3M US Trsy Note TR), 13.5% ST U.S. Fixed Income (ICE BofA 1-3Y US Corp&Govt TR), 21% Global Intermediate Bonds (FTSE WGBI Hdg USD), 10% U.S. Total Stock Market (Russell 3000 Index), 14% U.S. Large Value (Russell 1000 Value Index), 10% U.S. Small (Russell 2000 Index), 5% U.S. REITs (Dow Jones U.S. Select REIT Index), 13% Intl Large Value (MSCI World Ex USA Value Index (net div.)), 7% Intl Small (MSCI World Ex USA Small Index (net div.)), 6% Emerging Markets Value (MSCI Emerging Markets Value Index (net div)).

Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. Emerging markets involve additional risks, including, but not limited to, currency fluctuation, political instability, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal, and cannot be guaranteed against loss by a bank, custodian, or any other financial institution.

©Buckingham Strategic Partners 2020. All Rights Reserved. IRN R 18-287 (10/20)

This blog is for informational purposes only. It should not be retransmitted in any form without the express written consent of Delap Wealth Advisory, LLC, an investment advisor registered with the United States Securities & Exchange Commission. The contents of this communication should not be construed as investment advice intended for any particular individual or group of individuals. All information, statements, comments, and opinions contained in this blog regarding the securities markets or other financial matters is obtained (or based upon information obtained) from sources which we believe to be reliable and accurate. However, we do not warrant or guarantee the timeliness, completeness, or accuracy of any information or opinions presented herein. Any historical price or value is as of the date indicated. Information is provided as of the date of this material only and is subject to change without notice.