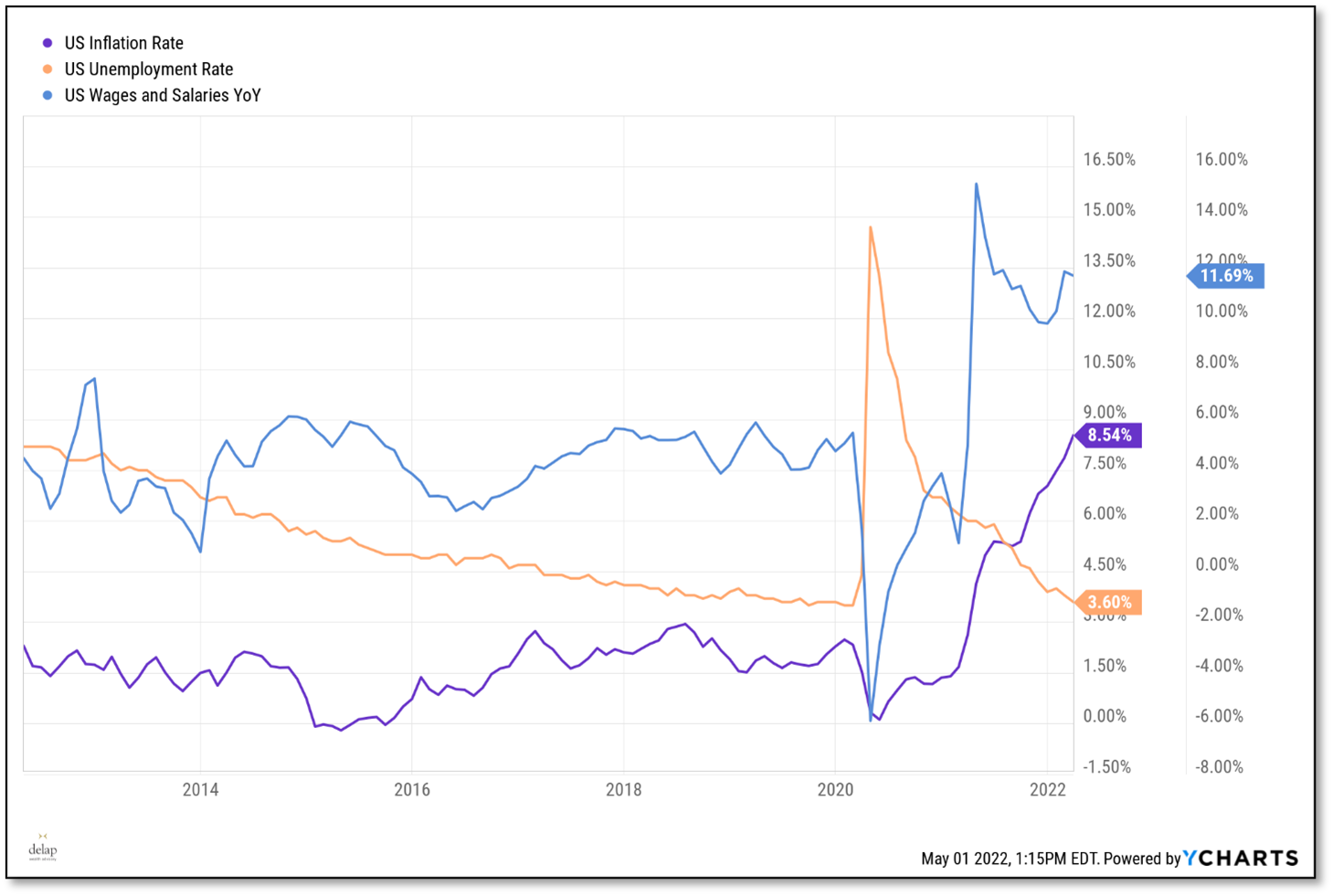

A recent spike in the U.S. inflation rate combined with wage growth and near-record low unemployment has captivated the attention of America as this information is integrated into current asset prices, causing markets to gyrate. At the time of this blog post, unemployment sits at just 3.6%, U.S. Inflation at 8.54%, and U.S. wage and salary year-over-year growth of 11.69%.

Figure 1: U.S. Inflation, Unemployment, and Wage Growth for 10 years

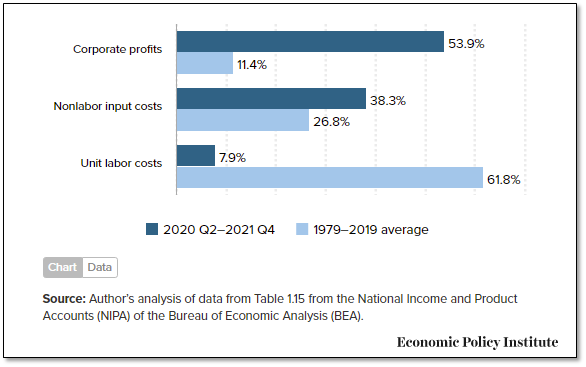

To better understand the current inflation we’re experiencing, let’s explore prices. The price of things in the U.S. economy generally can be broken into three categories: labor, nonlabor inputs, and mark-up (profits) over the first two components.

Figure 2: Normal and Recent Contributions to Growth in Unit Prices in the Nonfinancial Corporate Sector

A recent article published by the Economic Policy Institute points out that 53.9% of the price increases from Q2 2020-Q4 2021 were from corporate profits, which is a large increase compared to the 11.4% corporate profit average from 1979-2019. This is contrary to the recent narrative that current U.S. inflation is based purely on macroeconomic overheating. It’s worth noting that the Economic Policy Institute has roots in more leftist politics, and it receives a large portion of its funding from organized labor. That doesn’t change the fact that corporate pretax profits surged 25% year over year to $2.81 trillion, according to the Bureau of Economic Analysis. If discretionary price increases result in decreased demand, one would expect that profit-seeking companies will respond appropriately and some of the inflation pressures will dissipate.

The bottom line is that corporate America refinanced its debt at record low interest rates to lock in longer-term cheap financing and simultaneously enjoyed record profits to end 2021 with strong balance sheets.

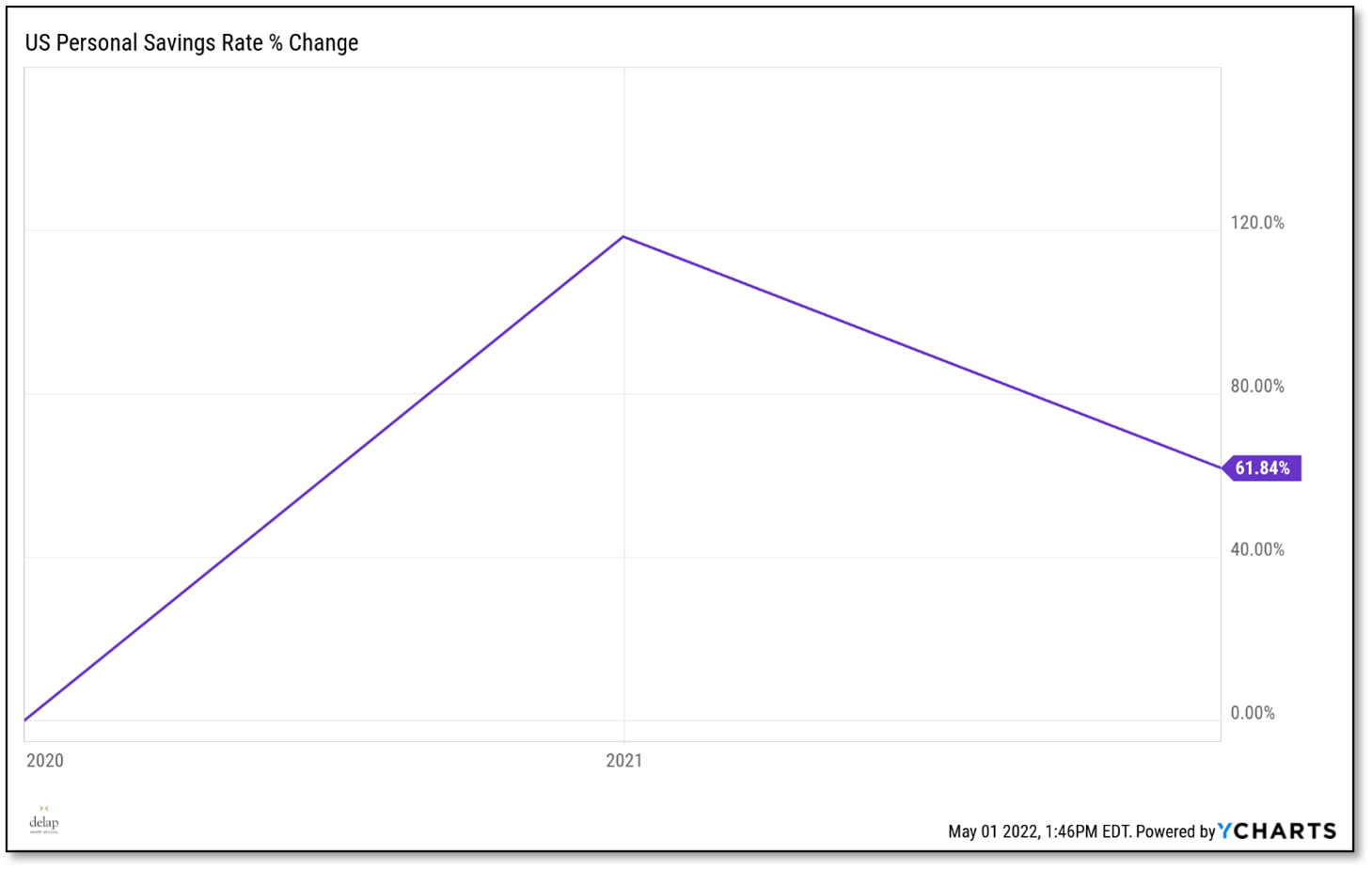

Figure 3: U.S. Personal Savings Rate Percent Change

Shifting our attention to the consumer, U.S. personal saving rates over the past 3 years have increased nearly 62%. The combination of pandemic shutdowns, remote work, stimulus payments, and a student loan pause all positively influenced savings accounts. Though 8% inflation is concerning to all, the U.S. consumer was financially strong going into 2022, and some of the financial sting has been offset by wage and salary increases.

We’ve seen over 7% inflation in 20 separate years here in the U.S. over the past 170 years. This current inflation isn’t unprecedented. Thinking back to economics class, we can be comforted by Adam Smith’s work and the observed resilience and adaptability of markets.

Ultimately, self-interested, profit-seeking individuals operate through a system of mutual interdependence to help move capital to where it will be treated best. This doesn’t mean there is an absence of risk today or certainty about the future. Rather, it’s acknowledging that both companies and individuals were strong going into these challenging times and that we’ve been here many times before as a country. Rather than responding emotionally, we can stand on the shoulders of financial and economic science to make more evidence-based decisions. As Corey Hoffstein of Newfound Research says, “Risk cannot be destroyed, only transformed.”

High inflation introduces or highlights risks that are often overlooked in more common economic times. Holding cash for a long-term need in the midst of 7%-plus inflation is risky. It’s a guaranteed way to lose purchasing power.

A common observable habit of successful stewards of wealth is that they focus more on the process (which they control) rather than recent results (which they don’t). By focusing more on good wealth habits and decision process, you’ll enjoy more predictable and scalable results. At some basic level, net worth can end up being a lagging measure of our financial habits.

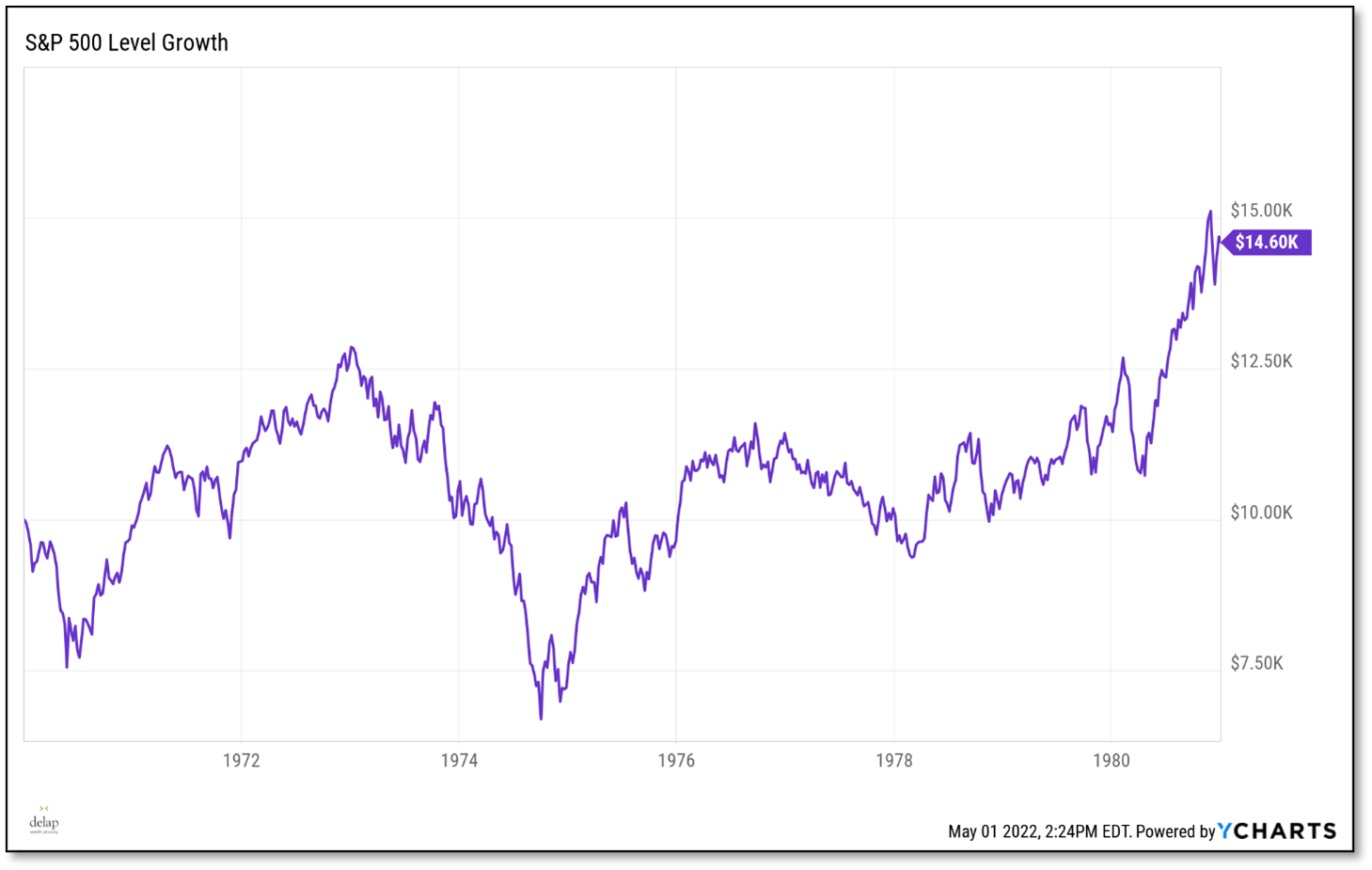

Figure 4: S&P 500 Level Growth

Looking at the most recent bout of inflation from January 1, 1970, through December 31, 1980, $10,000 invested in the S&P 500 still grew to $14,600. In real return terms (net of inflation) is that a spectacular return? No. However, for the forecast-focused investor who wanted to wait for a time where there was more certainty and less inflation (stagflation) what was the alternative?

The alternative was losing more than half of your purchasing power in less than a year. $10,000 dollars of cash on January 1, 1970, only purchased you $4,381 worth of goods by December 31, 1980. For this “safe” investor, the fear of quick pain (market correction) essentially guaranteed slow pain.

It’s always easier to measure real cost vs. an opportunity cost. Was the cortisol provoked by the uncertainty of the S&P well compensated when compared against the “safety” of cash? Absolutely! When asked about inflation, economist Thomas Sowell said, “It is a way to take people’s wealth from them without having to openly raise taxes. Inflation is the most universal tax of all.”

Ultimately, we prefer probabilistic thinking over stories. The former emphasizes uncertainty around future outcomes as well as in judging past outcomes. With our current inflation rate, what path forward offers a high probability of preserving and growing purchasing power and long-term wealth?

Since 1992, one-year returns on stocks have fluctuated widely. Yet the weakest returns can occur when inflation is low, and 23 of the past 30 years saw positive returns even after adjusting for the impact of inflation. From 1992 to 2021, the S&P 500 posted an average annualized return of 8.1% after adjusting for inflation. The annualized inflation-adjusted return on U.S. stocks is 7.3% when going all the way back to 1926.

History shows that stocks tend to outpace inflation over time — a valuable reminder for investors concerned that today’s rising prices will make it harder to reach their long-term financial goals. Alternative asset classes have also demonstrated respectable performance during inflationary times and rising rates.

In closing, we favor humble forecasts and bold diversification.

This blog is for informational purposes only. It should not be retransmitted in any form without the express written consent of Delap Wealth Advisory, LLC, an investment advisor registered with the United States Securities & Exchange Commission. The contents of this communication should not be construed as investment advice intended for any particular individual or group of individuals. All information, statements, comments, and opinions contained in this blog regarding the securities markets or other financial matters is obtained (or based upon information obtained) from sources which we believe to be reliable and accurate. However, we do not warrant or guarantee the timeliness, completeness, or accuracy of any information or opinions presented herein. Any historical price or value is as of the date indicated. Information is provided as of the date of this material only and is subject to change without notice.

Investing in securities involves the risk of loss, including the risk of loss of principal, which clients should be prepared to bear. No assurance is given that the investment objectives of any investment described in this communication will be achieved. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. The information contained in this blog is not intended as tax or legal advice, and Delap Wealth Advisory, LLC, does not provide any tax or legal advice to clients. You should consult with our firm or other independent financial, legal, and/or tax advisors before considering any investment or participation in any investment program.